VAT declaration line 080 filling procedure. Filling out a tax return. Filling out a VAT return

A VAT return is a standard reporting form that is filled out by VAT payers. How to correctly fill out a VAT return based on the results of the 1st quarter? In this material you will find step-by-step instructions with an example of filling out a declaration, general rules for filing reports, and you can also download a sample of filling out a VAT tax return and a blank form of the approved form.

Who is required to submit a VAT return in 2019

In accordance with paragraph 5 of Article 174 and paragraphs. 1 clause 5. Article 173 of the Tax Code of the Russian Federation for VAT the following are reported:

- organizations and individual entrepreneurs are VAT payers (firms and individual entrepreneurs that have switched to the simplified tax system, UTII, PSN, Unified Agricultural Tax or initially using these regimes do not pay this tax);

- tax agents;

- intermediaries who are not payers, who allocate VAT amounts in issued invoices.

It is handed over at the place of registration of the company or registration of the place of residence of the individual entrepreneur.

Deadline for filing VAT returns in 2019

In 2019, the deadlines are as follows:

Dates do not fall on weekends - there are no postponements. Thus, the deadline for submitting VAT for the 1st quarter of 2019 is April 25, 2019.

VAT return form for the 1st quarter of 2019

Approved by Order of the Federal Tax Service of Russia dated October 29, 2014 No. ММВ-7-3/, must be filled out taking into account the changes made by Order of the Federal Tax Service of Russia dated December 28, 2018 N SA-7-3/ The sample for filling out the VAT return for the first quarter of 2019 takes into account the changes made by the order .

The report consists of a title page and 12 sections. It is necessary to fill out only the first sheet and Section 1. The remaining parts are filled out if the necessary conditions are met.

Since 2014, taxpayers and tax agents have been filing returns electronically. Previously, the report was submitted on paper if the number of employees did not exceed 100 people. This opportunity cannot be used again. But in special cases, paper reporting is still submitted.

It can be submitted on paper:

- tax agents - non-payers of VAT (special regimes) or who have received exemption from its payment;

- organizations and individual entrepreneurs are non-payers of VAT or have received an exemption from paying it, if at the same time:

- they are not the largest taxpayers;

- the number of employees is not more than 100;

- they did not issue VAT invoices;

- did not work on the basis of agency agreements (in the interests of other persons) using invoices.

Exemption from the duties of a tax payer can be obtained if, over the previous three months, sales revenue does not exceed 2 million rubles.

Fine for failure to submit a declaration in 2019

Fine according to Article 119 of the Tax Code of the Russian Federation— 5% of the tax amount not paid on time. It is provided both for failure to submit reports and for submitting them in another form.

General rules for filling out the declaration

- Use only the approved form (if submitting on paper, filling out by hand or on a computer is acceptable - print only on one side of A4 sheet, do not staple).

- Enter one indicator in each line, starting from the left edge, and put dashes in the remaining empty cells.

- Indicate the amounts in full rubles, round up everything that is more than 50 kopecks, and discard anything less than 50 kopecks.

- Fill out text lines in capital block letters (if by hand, then in black, purple or blue ink, if on a computer, in Courier New font size 16-18).

Filling out a VAT return in 2019: step-by-step instructions

Example: how to fill out a VAT return for the 1st quarter of 2019.

Step 1 - Title Page

- The TIN and KPP of the company are indicated at the top of the page, then they are automatically duplicated on each sheet of the document;

- adjustment number when submitting the primary declaration - three zeros;

- tax period code for the 1st quarter - 21. Other codes: 22 - 2nd quarter; 23 - 3rd quarter; 24 - 4th quarter. When submitting a declaration monthly and when liquidating a company, the codes are different;

- reporting year 2019;

- Each tax office has a unique four-digit code; you can find it out by contacting the Federal Tax Service: the first two digits are the region code, the second two digits are the inspection code. The declaration is submitted to the Federal Tax Service at the place of registration of the taxpayer;

- the taxpayer enters a code at the place of registration, which depends on his status. Codes in Appendix 3 of the Order of the Federal Tax Service dated October 29, 2014 N ММВ-7-3/:

|

At the place of registration of individual entrepreneurs |

|

|

At the place of registration of the organization - the largest taxpayer |

|

|

At the place of registration of an organization that is not the largest taxpayer |

|

|

At the place of registration of the legal successor who is not the largest taxpayer |

|

|

At the place of registration of the legal successor - the largest taxpayer |

|

|

At the place of registration of the participant in the investment partnership agreement - the managing partner responsible for maintaining tax records |

|

|

At the location of the tax agent |

|

|

At the place of registration of the taxpayer when executing a production sharing agreement |

|

|

At the place of activity of the foreign organization through a branch of the foreign organization |

VESNA LLC is a Russian company that is not a major taxpayer. Enters code 214.

Filling algorithm:

- enter the name of the company in the longest field of the title page of the declaration, skipping one cell between the words;

- The code of the type of economic activity can be found using the classifier. VESNA LLC produces corrugated cardboard. You can find out more about which OKVED code to put in your VAT return for the 1st quarter of 2019 using Order of Rosstandart dated January 31, 2014 N 14-st;

- phone number;

- number of pages in the declaration. VESNA LLC submits a VAT return for the 1st quarter of 2019 on 18 sheets;

- At the bottom of the title page, enter the full name of the taxpayer or his representative, put the filing date and signature.

Step 2 - Section 1

Line by line:

- in line 010 of the 1st section of the declaration, enter the code OKTMO. For example - 45908000 - municipal district "Cheryomushki" of Moscow;

- 020 - KBK for VAT on goods (works, services) that are sold on the territory of the Russian Federation. You will find the KBK for VAT 2019;

- 030 - accrued VAT under clause 5 of Article 173 of the Tax Code of the Russian Federation. This is a tax that is paid when an invoice is issued to the buyer with VAT included by persons who are not its payers, or exempt from payment, or when goods are sold that are not subject to tax. VESNA LLC fills this field with dashes;

- 040 - the final value of Section 3 of the declaration;

- 050 - the sum of the total values from sections 4-6 of the declaration. VESNA LLC skips these sections - there is no tax base and tax payable at a zero rate, no amounts were generated for reimbursement from the budget in the quarter. There are dashes in the field;

- lines 060-080 are filled out only by participants in the investment partnership agreement (on the title page in the line “at the place of registration” code “227”). VESNA LLC puts dashes.

Section 2 is filled out by companies that act as tax agents. VESNA LLC skips this section.

Step 3 - Section 3

Line by line:

- 010-040 - tax base for the reporting quarter of 2019. LLC in the 1st quarter of 2019 sold goods that are taxed at a rate of 20%, therefore it fills out only line 010 in the declaration (in separate columns the tax base and the amount of VAT). In the remaining fields there are dashes;

- 070 - advance or other payments for upcoming deliveries of goods. During the reporting period, the organization received an advance against future supplies in the amount of 2,360,000 including VAT. In line 070, the tax base (1,800,000 rubles) and the tax itself (300,000 rubles) are entered separately in columns.

- 080-100 is a tax that is subject to restoration. In the example given, there are no such amounts - there are dashes in the fields;

- 105-109 - the amount of adjustments when selling goods, property rights or the enterprise as a whole.

- 110 - tax taking into account restoration (sum of the last columns of lines 010-080 of section 3 of the declaration);

- 120-185 - tax subject to deduction (Article 171 of the Tax Code of the Russian Federation, 172 of the Tax Code of the Russian Federation, clause 11 of Article 2 of the Protocol on Export and Import). In our example, line 120 is filled in - the amount of VAT paid when purchasing goods in the Russian Federation in accordance with Art. 171 of the Tax Code of the Russian Federation, as well as line 170. Please note that a new line 135 has appeared in the form.

- 190 - total deduction amount (sum of lines 120-180);

- 200 - the total amount of tax payable for the 1st quarter under section 3. The difference (positive) between the amount payable and the amount to be deducted is the difference between lines 110 and 190.

- 210 is the total amount to be reimbursed under section 3 of the VAT return for the 1st quarter of 2019. The line is filled in if the difference is negative.

The company fills out sections of the declaration from 4 to 6 when making sales in the reporting quarter, which are taxed at a preferential zero rate. Section 7 is issued for tax-free transactions, sales outside the territory of the Russian Federation, and prepayment of goods with a long production cycle. VESNA LLC did not carry out such operations in the 1st quarter of 2019.

Step 4 - Section 8

Section 8 contains values and data from the purchase book for received invoices, the right to deduction for which arose in the reporting period. VESNA LLC has the right to deduct VAT, which was presented by the counterparty seller and included in the issued invoice, from the total amount payable.

Continued from Section 8

Line by line:

- 001 is a dash, since the declaration is primary. To be completed only when submitting a specified form;

- 005 — transaction number in the purchase book;

- 010 — code for the type of transaction in the purchase book. In the above case, code 01 is indicated.

- 020 — invoice number presented by the seller;

- 030 - date of issue of the invoice;

- 040-090 - filled in when correcting an invoice or issuing an adjustment invoice;

- 100 — payment document number.

- 110 - date of drawing up the payment order;

- 120 - date of acceptance of the goods for registration.

- 130 - INN and checkpoint of the seller;

- 140 - INN and checkpoint of the intermediary - not filled in;

- 150 - the customs declaration number is entered only when importing goods from other countries. We put dashes;

- 160 - settlement with the seller was made in Russian currency;

- 170 - purchase price according to invoice including tax;

- 180 — tax amount in rubles;

- 190 - the total amount of tax deductible according to the purchase book in the 4th quarter.

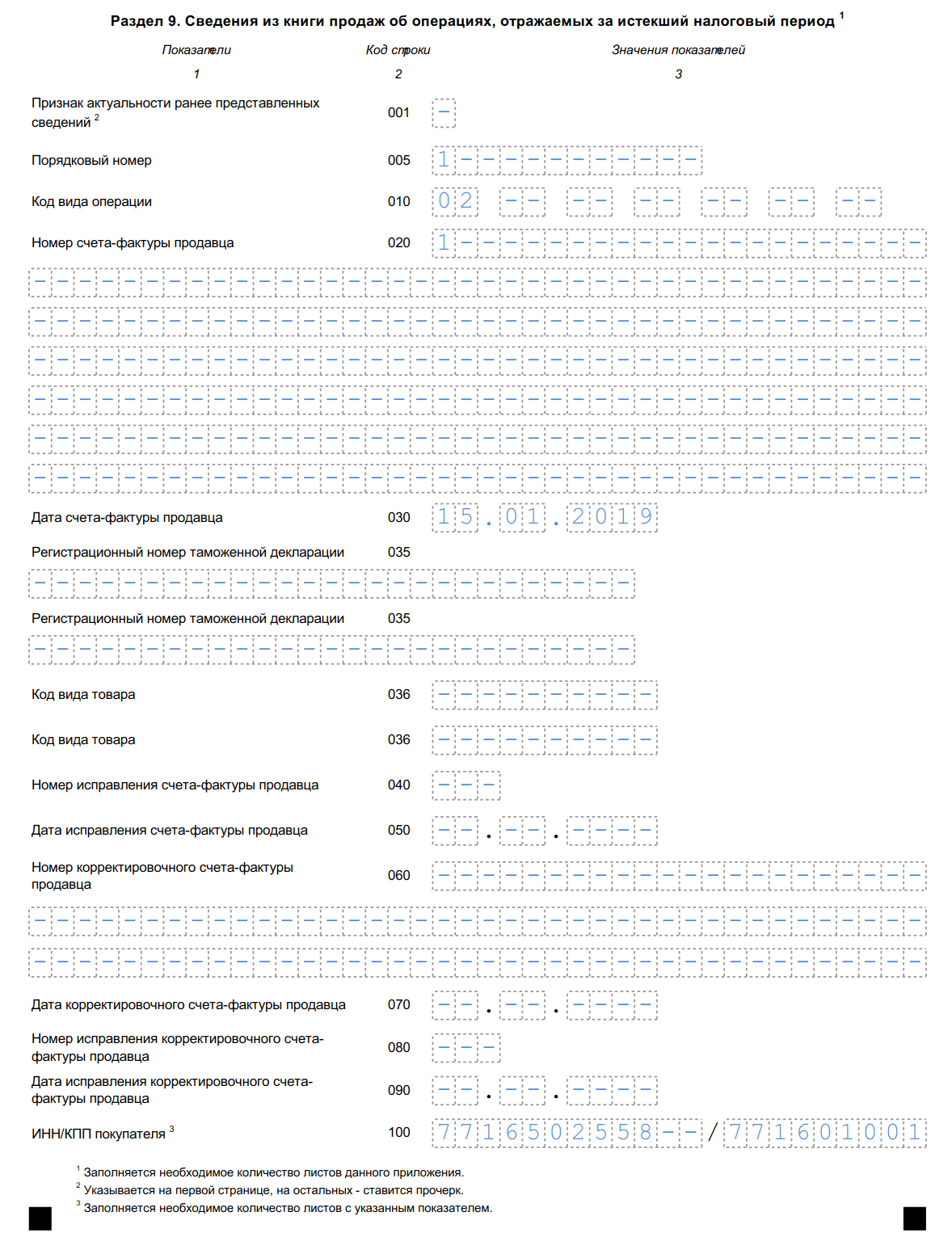

Step 5 - Section 9

Part 9 of the declaration includes information from the sales book - data on issued sales invoices that increase the tax base of the reporting quarter. It is imperative to reflect the prepayment for future delivery of goods in the amount of 2,360,000 rubles (including 18% VAT). The final page for the amount of transactions and tax is filled out once.

Section 9 on the first operation

Line by line:

- 001 - dash, since the declaration is primary (filled out only in the updated declaration);

- 005 — serial number of the transaction in the sales book;

- 010 — transaction type code in the sales book;

- 020 — number of the issued invoice;

- 030 — invoice date;

- 035 — registration number of the customs declaration;

- 036 (new line) - indicated during customs operations, codes are contained in the Commodity Nomenclature of the EAEU;

- 040-090 - fill in when correcting or issuing a corrective invoice;

- 100 - INN and checkpoint of the buyer.

- 110 - INN and checkpoint of the intermediary (not to be filled in);

- 120-130 - number and date of the payment document;

- 140 is the currency code.

- 150-160 — sales price including tax in the invoice currency and in rubles. Since the invoice is in rubles, we do not fill out line 150;

- 170-190 - sales cost without tax (separately at rates of 20, 18, 10 and 0%). All Section 9 transactions were carried out at a rate of 20%;

- 200-220 - the amount of VAT at rates of 20, 18 and 10% and the cost of sales exempt from tax. VESNA LLC fills in line 200.

Section 9 on second and subsequent operations

Almost completely duplicates the previous two pages, with the exception of the serial number of the transaction, date, buyer’s tax identification number and sale amount. For the third operation, code 02 from the sales book is indicated, since in this case the prepayment for upcoming deliveries is recorded. The filling principle is the same, but the values, dates and buyer details differ.

Section 9 Summary Indicators

- 230 — total cost of sales at a rate of 20% excluding VAT;

- 235 — total cost of sales at a rate of 18% excluding VAT

- 240 — total cost of sales — 10% excluding VAT;

- 250 — total cost of sales — 0% excluding VAT;

- 260 - tax at a rate of 20%;

- 265 - tax at the rate of 18%;

- 270 - tax at a rate of 10%;

- 280 is the amount exempt from tax.

Sections 10 and 11 of the declaration are filled out by commission agents and agents, developers, and companies working under a transport expedition agreement. Information is entered based on the invoice journal. Section 12 is issued by tax defaulters or persons exempt from paying it when they issue invoices with tax included. VESNA LLC leaves these sections blank.

VAT declaration for the 1st quarter of 2019, form (xls format)

You can fill out a declaration in online services on the websites of accounting software developers - My Business, Kontur, Nebo and others. Some sites allow you to do this freely, but usually the services require a small fee (up to 1000 rubles).

By the 20th day of the month following the tax period (quarter).

If the last day of the deadline for filing a declaration falls on a weekend and (or) a non-working holiday, then the end of the deadline is considered to be the next working day (Clause 7, Article 6.1 of the Tax Code of the Russian Federation).

The declaration can be submitted by the taxpayer in person, or through his representative, or by mail, or via telecommunications channels (electronically).

The day of submission of the declaration to the tax authority is considered (clause 8 of the Procedure for filling out the declaration):

- date of receipt by the tax authority when presented in person or through a representative;

- the date of sending the postal item with a description of the attachment when it was sent by mail;

- date of dispatch via telecommunication channels, recorded in the confirmation of a specialized telecommunications operator, when transmitted via telecommunication channels.

For persons selling goods (work, services) not subject to VAT or exempt from fulfilling the duties of a VAT taxpayer under Art. 145 of the Tax Code of the Russian Federation, the deadlines for filing, in case they issue an invoice indicating the VAT amounts, are established in clause 5 of Art. 174 Tax Code of the Russian Federation. These persons are required to submit a tax return by the 20th day of the month following the tax period (quarter).

For persons who are not VAT taxpayers, if they issue an invoice indicating the VAT amounts, the issue of the deadline for submitting a tax return is controversial.

According to para. 6 clause 3 of the Procedure for filling out the declaration, VAT defaulters are required to submit a declaration if they issue an invoice indicating the VAT amounts.

Meanwhile, the responsibility provided for in Art. 119 of the Tax Code of the Russian Federation, for failure to submit a declaration within the prescribed period cannot be applied to these categories, since they are not recognized as VAT taxpayers. As the courts indicate, persons who are not VAT payers do not fall under the concept of taxpayers (tax agents) listed in paragraph 5 of Art. 174 Tax Code of the Russian Federation. Therefore, they are not required to submit a declaration. See on this issue Resolution of the Federal Antimonopoly Service of the West Siberian District dated April 26, 2007 N F04-2469/2007(33681-A70-6), F04-2469/2007(33930-A70-6), Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated October 30, 2007 No. 4544/07 in case No. A65-6621/2006-CA1-7 and others.

According to clause 4 of the Procedure for filling out the declaration, the declaration is drawn up on the basis of sales books, purchase books and data from the accounting registers of the taxpayer (tax agent), and in cases established by the Tax Code of the Russian Federation, on the basis of data from the tax accounting registers of the taxpayer (tax agent).

The general requirements that must be observed when filling out the declaration are given in section. II Procedure for filling out the declaration. They are as follows.

The declaration is filled out with a ballpoint or fountain pen, black, purple or blue. It is allowed to print out the declaration on a printer.

Moreover, if the declaration is submitted on paper, then it is submitted only in the form of an approved machine-oriented form.

Correcting errors with a corrective agent is not acceptable. Double-sided printing of a paper declaration is not permitted. It is not allowed to staple the declaration sheets, leading to damage to the paper.

Only one indicator is indicated in each field of the declaration. If the indicator is missing, you must put a dash. The fields are filled in with numerical values from left to right.

The exception is for indicators whose values are a date, a proper fraction, or a decimal fraction. A proper fraction or decimal in an approved machine-oriented form corresponds to two fields separated by either a "/" (slash) or a "." (dot) respectively. The first field corresponds to the numerator of the proper fraction (the whole part of the decimal), the second - to the denominator of the proper fraction (the fractional part of the decimal).

Fractional numeric indicators are filled in similarly to the rules for filling in integer numeric indicators. A situation may arise when there are more cells for indicating the fractional part than numbers. Then in this case a dash is placed in the last free cells.

To indicate the date, three fields are used in order: day (field of two characters), month (field of two characters) and year (field of four characters), separated by a dot.

The declaration has continuous numbering, which is entered in the "Page" field. after filling out all the sheets.

The OKATO Code indicator, which has eleven cells, is reflected from the first cell. If the declaration is filled out manually, then the text fields are filled in with capital printed characters. Unfilled cells are crossed out. In this case, the dash is a straight line drawn in the middle of the free cells along the entire length of the field.

If the declaration is filled out by machine, then Courier New font with a height of 16 - 18 points is used.

According to paragraph 17 of section. II The procedure for filling out the declaration, all values of the cost indicators of the Declaration are indicated in full rubles. Indicator values are less than 50 kopecks. are discarded, and 50 kopecks. and more are rounded up to the full ruble.

The VAT return consists of the following sections:

Title page is filled out by the taxpayer, except for the section “To be filled out by a tax authority employee.”

The TIN and KPP are indicated on all sheets at the top of the declaration. If an organization’s TIN consists of 10 characters, then in the area reserved for recording the “TIN” indicator and consisting of 12 cells, zeros are entered in the first two cells.

TIN and KPP for a Russian organization are indicated according to:

- Certificate of registration with the tax authority of a legal entity formed in accordance with the legislation of the Russian Federation, at its location on the territory of the Russian Federation in form N 12-1-7, approved by Order of the Ministry of Taxes of Russia dated November 27, 1998 N GB-3-12/309;

- Certificate of registration of a legal entity with the tax authority at its location on the territory of the Russian Federation in form N 09-1-2, approved by Order of the Ministry of Taxes of Russia dated 03.03.2004 N BG-3-09/178.

INN and KPP for the largest taxpayers are indicated according to:

- Certificate of registration with the tax authority as the largest taxpayer of a legal entity formed in accordance with the legislation of the Russian Federation, in form N 9-KNS, approved by Order of the Ministry of Taxes of Russia dated August 31, 2001 N BG-3-09/319;

- Notification of registration with the tax authority of a legal entity as a major taxpayer in form N 9-KNU, approved by Order of the Federal Tax Service of Russia dated April 26, 2005 N SAE-3-09/178@.

INN and KPP for a foreign organization operating on the territory of the Russian Federation are indicated at the location of the branch of the foreign organization or at the location of the real estate and vehicles of the foreign organization that has real estate and vehicles on the territory of the Russian Federation, according to:

- Certificate of registration with the tax authority in form N 2401IMD;

- Information letter on registration with the tax authority of a branch of a foreign organization in form N 2201I, approved by Order of the Ministry of Taxes and Taxes of Russia dated April 7, 2000 N AP-3-06/124.

For an individual, the TIN is indicated in accordance with the Certificate of registration with the tax authority of an individual at the place of residence on the territory of the Russian Federation in form N 12-2-4, approved by Order of the Ministry of Taxes of Russia dated November 27, 1998 N GB-3-12/309, or in form N 09-2-2, approved by Order of the Ministry of Taxes and Taxes of Russia dated 03.03.2004 N BG-3-09/178.

When submitting the primary declaration in the area of the indicator "Adjustment number", code 0 is indicated in the first cell. If an updated declaration is submitted, then code 1 is indicated in the first cell.

In the "Tax period" zone, the code is indicated in accordance with the codes given in Appendix No. 3 to the Procedure for filling out the declaration. The code of the tax authority to which the Declaration is submitted is indicated in the documents given in paragraph 20 of section. III Procedure for filling out a tax return.

In the indicator "At the location (accounting) (code)" code 400 is indicated (at the place of registration of the taxpayer).

Below is the full name of the Russian organization (or the name of a branch of a foreign organization operating on the territory of the Russian Federation) in accordance with the constituent documents. If the taxpayer is an individual entrepreneur or an individual acting as a tax agent, then his last name, first name, patronymic (in full, without abbreviations, in accordance with the identity document) are indicated.

The code for the type of economic activity of the taxpayer is indicated in accordance with the All-Russian Classifier of Types of Economic Activities OK 029-2001 (OKVED), introduced by Resolution of the State Committee of the Russian Federation for Standardization and Metrology dated November 6, 2001 N 454-st.

In addition, the title page of the declaration indicates the taxpayer's contact telephone number, the number of pages on which the declaration is drawn up, and the number of sheets of supporting documents or copies thereof, including documents or copies thereof confirming the authority of the taxpayer's representative attached to the declaration.

For organizations, the accuracy and completeness of the information specified in the tax return is confirmed by the signature of the head of the organization, indicating his last name, first name, and patronymic. The date of signing the declaration is indicated and certified with a seal.

Individual entrepreneurs and individuals who are not recognized as individual entrepreneurs confirm the accuracy and completeness of the information with their signature and the date of signing.

If a tax return is submitted by a representative of the taxpayer - an individual or a legal entity, then in the "Representative" field, respectively, either the last name, first name, patronymic, or the full name of the organization is indicated.

When submitting a declaration by a taxpayer's representative - an individual, the personal signature of the taxpayer's representative, the date of signing, and also indicate the type of document confirming the authority of the taxpayer's representative.

When submitting a declaration by a representative of the taxpayer - a legal entity, the signature of the head of the authorized person, certified by the seal of the legal entity - the representative of the taxpayer, and the date of signing are affixed.

The line “Name of the document confirming the authority of the taxpayer’s representative” indicates the type of document confirming the authority of the taxpayer’s representative.

Section 1 "The amount of tax subject to payment to the budget (reimbursement from the budget), according to the taxpayer".

This section is required to be completed by all taxpayers. Line 030 “The amount of tax calculated for payment to the budget, in accordance with paragraph 5 of Article 173 of the Tax Code of the Russian Federation” is filled in in the case of issuing an invoice with the allocation of the amount by persons who are not VAT payers, are either exempt from paying tax, or sell goods (works, services) that are not subject to VAT. This amount is subject to payment to the budget according to a special rule in accordance with clause 4 of Art. 174 of the Tax Code of the Russian Federation, i.e. at the end of each tax period based on the corresponding sales of goods (work, services) for the expired tax period no later than the 20th day of the month following the expired tax period.

The OKATO code is indicated on line 010. It is filled out in accordance with the All-Russian Classifier of Objects of Administrative-Territorial Division OK 019-95, approved by Resolution of the State Standard of Russia dated July 31, 1995 N 413.

Line 020 indicates the budget classification code (KBK).

Line 040 indicates the amount of tax calculated for payment to the budget. Line 050 indicates the amount of tax to be refunded from the budget. Thus, lines 040 and 050 are filled in depending on the situation. The data specified in line 040 or 050 of section. 1 of the declaration, is formed according to the data reflected in section. 3 declarations.

When filling out lines 040 and 050, the following equalities must be met:

If ((page 230 section 3 + page 020 section 6) - (page 240 section 3 + page 010 section 4 + page 010 section 5 (according to group 3 and group 5) + page 030 section 6)) > or = 0, then line 040 is filled in.

If ((page 230 section 3 + page 020 section 6) - (page 240 section 3 + page 010 section 4 + page 010 section 5 (according to group 3 and group 5) + page 030 section 6))< 0, то заполняется строка 050.

If, as a result of calculations based on the results of the tax period, line 040 is filled in, then the tax must be paid to the budget in equal shares, no later than the 20th day of each of the three months following the expired tax period (clause 1 of Article 174 of the Tax Code of the Russian Federation).

Section 2 "The amount of tax payable to the budget according to the tax agent".

This section is completed only by persons performing the duties of a VAT tax agent.

Section 2 is filled out separately by the tax agent:

- for each foreign person who is not registered with the tax authorities as a taxpayer;

- for each lessor (state authority and management body and local government body leasing federal property, property of constituent entities of the Russian Federation and municipal property);

- for each seller in accordance with an agreement providing for the sale (transfer) of state property not assigned to state enterprises and institutions, constituting the state treasury of the Russian Federation, the treasury of a republic within the Russian Federation, the treasury of a territory, region, federal city, autonomous region, autonomous district, as well as municipal property not assigned to municipal enterprises and institutions, constituting the municipal treasury of the corresponding urban, rural settlement or other municipal entity;

- for each debtor when selling his property during bankruptcy proceedings in accordance with the legislation of the Russian Federation.

If there are several agreements for one person (foreigner, lessor, seller, etc.), then Section. 2 is filled out on one page.

According to paragraphs 3 and 4 of Art. 174 of the Tax Code of the Russian Federation, tax agents submit a declaration and pay tax at their location or at the place of residence of an individual (for individual entrepreneurs).

It is worth remembering that if the tax agent is unable to withhold the tax, then he is obliged to inform the tax authority about the impossibility of withholding the tax and the amount of the taxpayer’s debt.

On line 010, the authorized branch of a foreign organization registered with the tax authorities as a taxpayer indicates the checkpoint of the branch of the foreign organization for which the authorized branch represents Sec. 2 declarations and pays tax.

On line 020, the tax agent indicates the name of the payer (a foreign organization that is not registered; the lessor - a government body; the seller of state property; the debtor when selling property during bankruptcy proceedings).

The exception is sellers of confiscated property, property sold by court decision in accordance with clause 4 of Art. 161 of the Tax Code of the Russian Federation (with the exception of bankruptcy proceedings), and sellers of ships in accordance with clause 6 of Art. 161 Tax Code of the Russian Federation. These categories do not fill in line 020.

If the person indicated in line 020 has a TIN, it is listed in line 030.

Lines 040 and 050 indicate KBK and OKATO, respectively.

Line 070 indicates the code of the operation carried out by tax agents. The codes are indicated in accordance with Appendix No. 1 to the Procedure for filling out the declaration.

The amount of tax calculated by the tax agent for payment to the budget is indicated on line 060.

When purchasing goods (work, services) from foreign persons who are not registered with the tax authorities of the Russian Federation, tax agents determine the tax base in accordance with clause 1 of Art. 161 of the Tax Code of the Russian Federation, i.e. as the amount of income from the sale of goods (works, services) including tax. The tax base is determined for each transaction with a foreign person.

When determining the tax base, the tax agent also needs to remember that if he paid for goods (work, services) in foreign currency, then his expenses for the purchase of goods (work, services) are recalculated into rubles on the date of shipment or on the date of payment, depending on what happened earlier (clause 3 of article 153 of the Tax Code of the Russian Federation). The tax rate is assumed to be 18/118 (clause 4 of Article 164 of the Tax Code of the Russian Federation).

Tax agents purchasing work and services from foreign organizations that are not registered with the tax authorities of the Russian Federation, on line 060 indicate the amount of VAT that was paid to the budget simultaneously with the payment of funds to the foreign organization in accordance with clause 4 of Art. 174 of the Tax Code of the Russian Federation (paragraph 3, clause 37.6 of the Procedure for filling out the declaration). The exception is non-cash forms of payment.

When leasing state and municipal property, the tax agent determines the tax base as the amount of rent including tax (clause 3 of Article 161 of the Tax Code of the Russian Federation). The tax base is determined by the tax agent separately for each leased property. The tax amount is determined by the tax agent when paying the rent, that is, either at the time of prepayment (partial payment) for purchased services, or at the time of payment (partial payment) for already purchased services. The estimated tax rate is applied - 18/118 (clause 4 of article 164 of the Tax Code of the Russian Federation).

When acquiring state and municipal property, the tax agent determines the tax base as the amount of income from the sale (transfer) of this property, taking into account tax. The tax base is determined separately for each transaction involving the sale (transfer) of the specified property. The tax amount is determined by the tax agent when paying for the property, that is, at the time of advance payment (partial payment) of the acquired property or at the time of payment (partial payment) of the already acquired property. The estimated tax rate is applied - 18/118 (clause 4 of article 164 of the Tax Code of the Russian Federation).

When selling confiscated property or property sold by court decision on the territory of the Russian Federation, the tax agent determines the tax base based on the market price of the property (valuables) being sold. The tax rate is 18% (clause 3 of Article 164 of the Tax Code of the Russian Federation). The tax base is determined, as in normal sales, on the date of shipment and (or) receipt of advance payment for future deliveries.

When selling goods (work, services) to foreign persons who are not registered with the tax authorities of the Russian Federation, under intermediary agreements, the tax agent determines the tax base as the cost of such goods (work, services), property rights, taking into account excise taxes (for excisable goods) and without inclusion of the tax amount in them (clause 5 of Article 161 of the Tax Code of the Russian Federation).

The moment the tax base is determined is the earliest of the following dates:

- day of shipment (transfer) of goods (works, services), property rights;

- day of payment, partial payment for upcoming deliveries of goods (performance of work, provision of services), transfer of property rights.

The tax rate, the VAT rate, is 18% or 10% (clauses 2, 3, Article 164 of the Tax Code of the Russian Federation).

It is worth noting that for the last two categories (when selling confiscated property and when selling goods of foreign persons under intermediary agreements), line 060 is filled out in a special order.

Thus, line 080 indicates the amount of tax calculated by the tax agent on goods shipped (work, services, property rights).

Line 090 indicates the amount of tax calculated by the tax agent from the payment received (partial payment) towards the upcoming shipment (performance of work, provision of services, transfer of property rights). In other words, line 090 indicates “advance” VAT.

Line 100 is filled in if the moment of determining the tax base was the day of payment (partial payment) for upcoming deliveries in the previous tax period, and the day of shipment (performance of work, provision of services, transfer of property rights) falls on the next (i.e. current) taxable period. Thus, line 100 is filled in in the current quarter if in the previous tax return in section. 2 on line 090 the amount of “advance” VAT was indicated. In other words, VAT paid on the advance payment is deductible. A deduction is possible in a proportion not exceeding the amount of tax calculated upon shipment of goods (performance of work, provision of services, transfer of property rights), for the upcoming delivery of which an advance payment was received (clause 37.8 of the Procedure for filling out the declaration).

Therefore, line 060 will be filled in as follows:

Line 060 = page 090 if line 080 = 0

or

Line 060 = page 080 if line 090 = 0.

If in previous quarters a value was indicated on line 090 (i.e., advance tax was calculated), then

line 060 = (page 080 + page 090) - page 100.

Section 3 "Calculation of the amount of tax payable to the budget for transactions taxed at the tax rates provided for in paragraphs 2 - 4 of Article 164 of the Tax Code of the Russian Federation."

This section is filled out by VAT taxpayers who carry out transactions taxed at rates 10, 18 and the settlement rate (18/118 or 10/110).

Conditionally Sec. 3 can be divided into two parts:

- the first reflects transactions related to the calculation of VAT on various objects;

- the second reflects tax deductions.

Lines 010 - 040 reflect the tax base (column 3) and the amount of calculated VAT (column 5) on goods shipped (work performed, services rendered). The tax base in this case is equal to the cost of shipped goods (work, services, property rights). The tax rate is applied depending on the type of goods (work, services) sold - 10%, 18% or the estimated rate.

Operations are not reflected on lines 010 - 040:

- not subject to taxation (exempt from taxation) in accordance with Art. 149 Tax Code of the Russian Federation;

- not recognized as an object of taxation in accordance with Art. 146 Tax Code of the Russian Federation;

- the place of sale of which is not recognized as the territory of the Russian Federation in accordance with Art. Art. 147 - 148 Tax Code of the Russian Federation;

- taxed at a rate of 0 percent (including in the absence of confirmation of the validity of its application).

In addition, lines 010 - 040 also do not reflect the amounts of payment, partial payment received on account of upcoming deliveries of goods (performance of work, provision of services).

The amount of VAT calculated for the transactions specified in pages 010 - 040 is indicated in column 5.

In this case, it is calculated as follows:

- Line 010 columns 5 = line 010 gr. 3 x 18%.

- Line 020 columns 5 = line 020 gr. 3 x 10%.

- Line 030 columns 5 = line 030 gr. 3 x 18/118.

- Line 040 columns 5 = line 040 gr. 3 x 10/110.

Line 050 indicates the tax base for the sale of the enterprise as a property complex in column 3, and the amount of calculated VAT in column 5. The tax base in this case is determined separately for each type of asset of the enterprise (clause 1 of article 158 of the Tax Code of the Russian Federation). The tax rate applies in the amount of 15.25% (regardless of which asset of the enterprise is sold). The exception is property, the sale of which is not subject to VAT in accordance with Art. 149 of the Tax Code of the Russian Federation. VAT is not calculated on it.

Line 060 indicates in column 3 the cost of construction and installation work performed for own consumption, in column 5 - the amount of calculated VAT. The tax base is defined as the cost of construction and installation work performed for one’s own consumption, calculated on the basis of all actual expenses of the taxpayer for their implementation (clause 2 of Article 159 of the Tax Code of the Russian Federation).

The moment of determining the tax base when performing construction and installation work for one’s own consumption in accordance with clause 10 of Art. 167 of the Tax Code of the Russian Federation is the last date of each tax period. The tax rate is assumed to be 18%.

On line 070, column 3 indicates the amount of payment, partial payment received on account of upcoming deliveries of goods (work, services), transfer of property rights, and in column 5 - the amount of calculated VAT.

Line 070 is not filled in when selling goods (work, services) with a production cycle of more than 6 months, if the organization has exercised the right granted by clause 13 of Art. 167 Tax Code of the Russian Federation.

The legal successors also indicate on line 070 the amounts of advances received from the reorganized (reorganized) organization.

The tax base when receiving an advance is determined as the amount of payment received, including VAT (paragraph 2, clause 1, article 154 of the Tax Code of the Russian Federation). The estimated tax rate is accepted.

Line 070 columns 5 = line 070 columns 3 x 18/118 + page 070 columns 3 x 10/110.

Line 080, column 3 reflects the amounts associated with settlements for payment of taxable goods (work, services), and column 5 - the amount of calculated VAT.

The tax base in this case is determined in accordance with paragraph 1 of Art. 162 of the Tax Code of the Russian Federation. The estimated tax rate is accepted.

Lines 090 - 110 indicate the tax amounts subject to recovery.

It should be noted here that line 090 indicates all VAT amounts subject to recovery. Line 100 reflects the amounts of VAT that were taken for deduction in previous periods and are now subject to restoration in connection with transactions for the sale of goods (works, services) taxed at a rate of 0%.

Line 110 reflects the amount of VAT that is subject to restoration for payment to the budget in cases of change in the terms (or termination) of the contract and the return of advance amounts under this contract (if VAT on the advance was accepted for deduction), as well as in the event of the right to deduct on shipped goods. goods, if “advance” VAT was previously accepted for deduction for the corresponding transaction (clause 3, clause 3, article 170 of the Tax Code of the Russian Federation).

Line 120 in column 5 reflects the total amount of VAT for the expired tax period:

Line 120 = page 010 + page 020 + page 030 + page 040 + page 050 + page 060 + page 070 + page 080 + page 090.

Lines 130 - 210 reflect the amounts of tax subject to deduction in accordance with Art. Art. 171, 172 of the Tax Code of the Russian Federation, as well as in accordance with paragraph 8 of section. I “The procedure for applying indirect taxes when importing goods” Provisions on the procedure for collecting indirect taxes and the mechanism for monitoring their payment when moving goods between the Russian Federation and the Republic of Belarus.

Line 130 reflects:

- amounts of “input” VAT on goods (work, services), property rights, fixed assets, equipment for installation, intangible assets for carrying out taxable transactions (clause 2 of Article 171, clause 1 of Article 172 of the Tax Code of the Russian Federation);

- the amount of tax paid on business trip expenses and entertainment expenses accepted for deduction when calculating corporate income tax (clause 7 of Article 171 of the Tax Code of the Russian Federation);

- amounts of “input” VAT that were previously restored by the shareholder (participant) upon receipt of property, intangible assets and property rights as a contribution (contribution) to the authorized (share) capital (fund) (clause 11 of Article 171 of the Tax Code of the Russian Federation);

- the amount of tax previously calculated from advance payments and paid to the budget upon termination of the contract (change of conditions) and return of the advance to the buyer (clause 5 of Article 171, clause 4 of Article 162.1 of the Tax Code of the Russian Federation);

- amounts of “input” VAT on goods (work, services), fixed assets, intangible assets, property rights used to carry out operations with a long production cycle (clause 7 of Article 172 of the Tax Code of the Russian Federation);

- the amount of “input” VAT from contractors on goods (work, services) purchased for construction and installation work, as well as the amount of “input” VAT when purchasing unfinished capital construction projects (clause 6 of Article 171 of the Tax Code of the Russian Federation).

Line 140 reflects the amounts of “input” VAT from contractors (customers-developers) when they carry out capital construction of fixed assets, accepted for deduction in the manner specified in clause 5 of Art. 172 of the Tax Code of the Russian Federation, and taking into account the features established by Art. 3 of the Federal Law of July 22, 2005 N 119-FZ.

In this case, we are talking about the amounts of “input” VAT on contract work during capital construction completed before 01/01/2006 (Parts 1, 2, Article 3 of the Federal Law of July 22, 2005 N 119-FZ).

The amounts reflected on line 140 are taken into account in the total amount of deductions reflected on line 130.

On line 150, buyers indicate the VAT amounts presented by sellers when transferring advance payments. The deduction is made on the basis of clause 12 of Art. 171 and paragraph 9 of Art. 172 of the Tax Code of the Russian Federation. Subsequently, the restoration of VAT from advances is carried out according to line 110 of section. 3.

When filling out lines 110 and 150 of section. 3, questions may arise regarding deliveries for which both advance payments and shipment took place in the same tax period. There are no specific features in the Procedure for filling out the declaration for such supplies and transactions. There are two options for filling lines 110 and 150:

- Line 150 reflects all VAT amounts on advances, incl. and for transactions “closed” during the quarter. Accordingly, line 110 also indicates all amounts of restored VAT from the advance, incl. and for transactions “closed” during the quarter. This option is good because the indicators of the Purchase Book and the Sales Book for the reporting quarter will correspond to the declaration indicators for the same period.

- Line 150 reflects only VAT amounts on “unclosed” advances. In other words, line 150 reflects only the balance of settlements with the budget. Line 110 will reflect only the VAT amounts subject to recovery in the reporting period for supplies of previous periods. This option is less labor intensive and simple.

Line 160 indicates the amount of VAT on construction and installation work performed for own consumption. According to para. 2 clause 5 art. 172 of the Tax Code of the Russian Federation, deductions of accrued VAT on construction and installation work performed for one’s own consumption are made in the same tax period when it was accrued. In other words, the amounts of VAT on construction and installation work performed for own consumption are reflected in the reporting (tax) period in section. 3 on both line 060 and line 160.

Lines 170 - 190 reflect the amounts of VAT paid when importing goods into the customs territory of the Russian Federation. The list of goods not subject to taxation (exempt from taxation) is provided for in Art. 150 Tax Code of the Russian Federation.

Line 180 indicates the amount of VAT paid at customs on all goods, line 190 indicates the amount of VAT paid when importing goods from the Republic of Belarus (clause 8 of section I of the Regulations on the procedure for collecting indirect taxes and the mechanism for monitoring their payment when moving goods between the Russian Federation and the Republic of Belarus).

In this case the equality must be satisfied:

Line 170 = page 180 + page 190.

On line 200, the seller reflects the amounts of VAT previously calculated from prepayment amounts and accepted for deduction in accordance with clause 6 of Art. 172 of the Tax Code of the Russian Federation in the reporting period in connection with the fulfillment of obligations for the shipment of goods (performance of work, provision of services). For a reorganized (reorganized) organization, line 200 is filled in after the debt is transferred to the legal successor (clause 1 of Article 162.1 of the Tax Code of the Russian Federation).

The assignee on line 200 indicates the amounts of VAT calculated from advance payments by the reorganized (reorganized) organization, which are accepted for deduction after the date of sale of the relevant goods (work, services) (clauses 2 - 4 of Article 162.1 of the Tax Code of the Russian Federation).

The amounts of the advance received and the amount of VAT calculated on these amounts are reflected in line 070 of section. 3 during the period of receiving the advance. Then, after the goods (work, services) have been shipped, line 200 indicates the VAT amounts calculated from the advance payment amounts received previously.

Line 210 reflects the deductible amount of VAT actually transferred by the taxpayer to the budget as a buyer - tax agent.

Tax agents fill out line 210 in the following cases:

- acquisition of goods (work, services) from a foreign organization that is not registered with the tax authorities of the Russian Federation (clauses 1, 2 of Article 161 of the Tax Code of the Russian Federation);

- transfers of rent under lease agreements for state property concluded with state authorities and management bodies or with local government bodies (paragraph 1, clause 3, article 161 of the Tax Code of the Russian Federation);

- acquisition (transfer) of state property not assigned to a state or municipal enterprise (institution) and constituting the treasury of the Russian Federation, a constituent entity of the Russian Federation or the corresponding municipal entity (paragraph 2, paragraph 3, article 161 of the Tax Code of the Russian Federation).

Line 210 is also filled in by the tax agent when selling goods (work, services) in case of return of goods or refusal of goods (work, services) and in case of termination (change of conditions) of the contract and return of the advance (clause 5 of Article 171 of the Tax Code of the Russian Federation).

Line 210 indicates the amount of VAT reflected in line 060 of section. 2. In other words, VAT calculated by the tax agent is first indicated on line 060 of section. 2, and then this amount is accepted for deduction, and accordingly, is indicated on line 210 of section. 3.

According to the norms of paragraph 3 of Art. 171, art. 172 of the Tax Code of the Russian Federation, a tax agent has the right to deduct VAT in the tax period in which the actual payment of these tax amounts to the budget was made.

The Ministry of Finance of Russia in its Letters (dated 07/15/2009 N 03-07-08/151, dated 04/07/2008 N 03-07-08/84) also indicates that the deduction by the tax agent is made during the period of actual payment of VAT to the budget.

Arbitration practice in this matter supports the position of the Ministry of Finance of Russia (see Resolutions of the FAS Moscow District dated November 30, 2009 No. KA-A41/12049-09 in case No. A41-9169/09, FAS Volga District dated June 2, 2009 in case No. A55-17122 /2008, Federal Antimonopoly Service of the West Siberian District dated May 24, 2006 N F04-3085/2006 (22778-A27-26) in case N A27-34349/05-6).

Line 220 is the final line for calculating the amounts of VAT subject to deduction.

Line 220 = page 130 + page 150 + page 160 + page 170 + page 200 + page 210.

Lines 230 and 240 reflect the amount of tax payable to the budget or the amount of tax to be reduced, respectively, calculated under section. 3.

If page 120 - page 220 > or = 0, then line 230 is filled in.

If page 120 - page 220< 0, то заполняется строка 240.

The values of indicators of lines 230 and 240 are involved in calculating the values of indicators of lines 040 and 050 of section. 1 (paragraph 3, clause 34.3 and paragraph 2, clause 34.4 of the Procedure for filling out the declaration).

Appendix No. 1 to section. 3 “The amount of VAT subject to recovery and payment to the budget for the reporting year and previous reporting years.”

This Appendix is filled out only once a year (simultaneously with the declaration for the last tax period of the calendar year). The Appendix is completed in cases of restoration of VAT amounts previously accepted for deduction on property in respect of which construction and installation work was carried out, the property was used for VAT-taxable operations (accordingly, a tax deduction was applied under clause 6 of Article 171 of the Tax Code of the Russian Federation), when in the future, such property is used to carry out the operations specified in paragraph 2 of Art. 170 of the Tax Code of the Russian Federation, i.e. begins to be used in VAT-free activities.

In this case we are talking about the following property:

- real estate objects (fixed assets) built during capital construction by contractors;

- acquired real estate objects (except for aircraft, sea vessels and inland navigation vessels, as well as space objects);

- construction and installation work for own consumption, during which the taxpayer calculated the amount of tax payable to the budget.

However, there are two exceptions to this rule (there is no need to restore VAT):

- fixed assets that are fully depreciated;

- At least 15 years have passed since the commissioning of fixed assets for this taxpayer. It should be borne in mind that fixed assets must be kept and used by a given taxpayer for 15 years, and not just be 15 years old.

Accordingly, for fully depreciated facilities and for facilities where more than 15 years have passed since their commissioning, Appendix No. 1 to Section. 3 is not filled in.

According to para. 5 paragraph 6 art. 171 of the Tax Code of the Russian Federation, restoration is carried out within 10 years, starting from the year in which depreciation began to accrue on this property. The amount of VAT subject to recovery in each year (out of ten years) is determined as 1/10 of the amount of tax accepted for deduction, in the share attributable to non-taxable transactions, calculated for each of these ten years.

The application is completed for each property (fixed asset). For example, if a taxpayer began to use two fixed assets in non-VAT taxable activities, then two Appendices No. 1 to Section. 3.

For real estate objects put into operation before 01/01/2006, the procedure is clause 6 of Art. 171 of the Tax Code of the Russian Federation does not apply. Consequently, VAT on such objects must be restored in accordance with paragraph 3 of Art. 170 of the Tax Code of the Russian Federation, i.e. lump sum and in proportion to the residual value of the object.

Lines 010 - 070 indicate data about the object (its name, location address, commissioning date, depreciation start date, cost of the object and the amount of VAT accepted for deduction). At the same time, the data in lines 010 - 070 does not change throughout the entire period of restoration of tax amounts.

On line 030, transaction codes are indicated in accordance with Appendix No. 1 to the Procedure for filling out the declaration.

Line 040 (date of commissioning) is filled in according to accounting data.

The date indicated on line 050 (the start date of depreciation) must coincide with the date indicated in the first line of column 1 on line 080. On line 060, the cost of the object is indicated excluding VAT amounts.

In column 1, line 080, the first line indicates the calendar year in which depreciation began to be calculated according to tax accounting data. In subsequent calendar years, calendar years are indicated in this column in ascending order.

Column 2 on line 080 reflects the date of commencement of use of the property in non-VAT taxable activities.

If during the calendar year the object was not used in activities not subject to VAT, then dashes are added on line 080 in columns 2 - 4.

Column 3 on line 080 indicates the share of goods (work, services) shipped in the calendar year, property rights that are not subject to VAT and specified in clause 2 of Art. 170 of the Tax Code of the Russian Federation, in the total cost of goods (work, services) shipped in a calendar year. The share is indicated as a percentage and is rounded to the nearest decimal place.

Column 4 on line 080 reflects the amount of VAT subject to recovery and payment to the budget on the property for the calendar year for which Appendix No. 1 is drawn up:

Line 080 columns 4 = line 070 x 1/10 x line 080 columns 3 / 100.

The amount of VAT reflected on line 080 of column 4 for the calendar year for which the tax is restored (and therefore the Appendix is filled out) is transferred to line 090 of section. 3 for the last tax period.

Appendix No. 2 to section. 3 “Calculation of the amount of tax calculated for transactions involving the sale of goods (works, services), transfer of property rights, and the amount of tax subject to deduction by a foreign organization carrying out business activities on the territory of the Russian Federation through its divisions (representative offices, branches).”

This Appendix is completed only by foreign organizations registered with the tax authorities as a taxpayer.

According to paragraph 3 of Art. 144 of the Tax Code of the Russian Federation, foreign organizations that have several divisions (representative offices, branches) on the territory of the Russian Federation independently choose a division at the place of tax registration of which they will submit tax returns and pay taxes. A foreign organization is obliged to notify the tax authorities in writing at the location of its branches registered in the Russian Federation.

Accordingly, Appendix No. 2 is filled out and submitted by the authorized branch of the foreign organization at its location. Appendix No. 2 is a kind of transcript of section. 3, given for each division of a foreign organization.

Column 1 indicates the checkpoint of each division of a foreign organization registered with the tax authorities, operations for the sale of goods (works, services) of which are reflected in the declaration.

Column 2 indicates the amount of VAT calculated on transactions subject to taxation carried out by the relevant department. This includes the amounts of recovered VAT.

Column 3 indicates the amount of tax deductions attributable to the corresponding division.

When filling out columns 2 and 3, the following equations must be observed:

- Sum of values in column 2 = page 120 section. 3.

- Sum of values in column 3 = page 220 section. 3.

Section 4 "Calculation of the amount of tax on transactions involving the sale of goods (works, services), the validity of applying a tax rate of 0 percent for which is documented."

This section is filled out by taxpayers carrying out export operations, as well as work and services related to the production and sale of goods for export, who have collected the necessary package of documents within the period established by paragraph. 1 clause 9 art. 165 of the Tax Code of the Russian Federation - within 180 days.

For the period from July 1, 2008 to March 31, 2010 inclusive, the period for confirmation of export is 270 calendar days (i.e. increased by 90 days). Corresponding changes have been made to clause 9 of Art. 165 of the Tax Code of the Russian Federation, clause 1, art. 1 of the Federal Law of December 27, 2009 N 368-FZ.

The moment of determining the tax base for the export of goods is the last day of the month in which the package of documents is collected (clause 9 of Article 167 of the Tax Code of the Russian Federation). When the package of documents is collected, section is submitted. 4 tax returns. According to paragraph 10 of Art. 165 of the Tax Code of the Russian Federation, documents confirming the tax rate are submitted simultaneously with the tax return.

Documents that must be submitted simultaneously with the declaration:

- a contract (copy of a contract) of a taxpayer with a foreign person for the supply of goods (supplies) outside the customs territory of the Russian Federation.

- bank statement (copy of the statement) confirming the actual receipt of proceeds from the sale of the specified goods (supplies) to a foreign person to the taxpayer’s account in a Russian bank.

- a customs declaration (its copy) with marks from the Russian customs authority that released the goods under export regime, and the Russian customs authority in the region of whose activity there is a checkpoint through which the goods were exported outside the customs territory of the Russian Federation;

- copies of transport, shipping and (or) other documents with marks from border customs authorities confirming the export of goods outside the territory of the Russian Federation.

In column 1 section. 4 reflects transaction codes in accordance with Appendix No. 1 to the Procedure for filling out the declaration.

Column 2 for each transaction code reflects the tax bases for the expired tax period for which the declaration is submitted, taxed at a tax rate of 0%. The tax base is equal to the cost of goods sold (work, services), for which there is confirmation of a 0% rate.

Column 3 for each code reflects the amount of “input” VAT on goods (work, services, property rights) used in the sale of goods (work, services), for which the validity of applying a 0% rate has been confirmed. Column 3 reflects:

- the amount of tax paid by the taxpayer when importing goods into the customs territory of the Russian Federation;

- tax amounts previously calculated from the amounts of payment received before January 1, 2006, partial payment for upcoming deliveries of goods (performance of work, provision of services), counted in the tax period when selling goods (work, services), justification for applying a tax rate of 0 percent which has been documented.

Column 4 for each transaction code indicates the amount of tax previously calculated for export transactions for which the validity of applying a 0% rate has not been confirmed. According to para. 2 clause 9 art. 165, para. 2 clause 9 art. 167 of the Tax Code of the Russian Federation, if within 180 days (in the period from 07/01/2008 to 01/01/2011 - 270 days) the taxpayer does not confirm the right to apply the 0% rate, i.e. does not collect a complete package of documents, he is obliged to charge VAT at a rate of 18%. This tax amount is reflected in column 3 of section. 6 declarations for the period in which the application of the 0% rate was not confirmed (i.e. for the period in which 180 (90) calendar days have expired from the date of shipment).

Column 5 for each transaction code indicates the amount of VAT previously accepted for deduction on goods (works, services) for which the validity of applying a tax rate of 0 percent has not previously been documented. This tax amount is reflected in column 4, section. 6 previous tax periods (i.e. for the period in which 180 (90) calendar days have expired from the date of shipment).

Line 010 is the final line. It calculates the total amount of tax accepted for deduction on transactions of sale of goods (works, services), the validity of applying a 0% rate for which has been confirmed.

Line 010 = sum of values in column 3 + sum of values in column 4 - sum of values in column 5.

The indicator of line 010 is taken into account when calculating the indicators of lines 040 and 050 of section. 1 (paragraph 3, clause 34.3 and paragraph 2, clause 34.4 of the Procedure for filling out the declaration).

Section 5 “Calculation of the amount of tax deductions for transactions involving the sale of goods (works, services), the validity of applying a tax rate of 0 percent for which was previously documented (not confirmed).”

This section is filled out by taxpayers carrying out export operations, as well as work and services related to the production and sale of goods for export, for which the validity of applying the 0% rate was confirmed (not confirmed) in previous tax periods, and the right to apply tax deductions for these operations arose only in the current period, i.e. the period for which the declaration is submitted.

Section 5 is completed for each tax period in which the validity of applying the zero rate was confirmed (not confirmed), but the right to tax deductions has not yet arisen.

The details “Reporting year” and “Tax period” reflect the data on the year and tax period indicated on the title page of the declaration for the corresponding period (i.e. the declaration in which export transactions were previously reflected, the justification for applying a 0% rate for which was confirmed).

Column 2 for each transaction code reflects the tax bases for transactions involving the sale of goods (works, services), taxed at a rate of 0%, the validity of which for these transactions is documented in the period indicated by the details “Reporting year” and “Tax year”. period".

Column 3 reflects tax deductions for each transaction code, i.e. the amount of “input” VAT on goods (works, services, property rights) purchased for the sale of exported goods (works, services). The validity of applying a 0% rate for these transactions was documented in the period indicated by the details “Reporting year” and “Tax period”, and the right to include “input” VAT in tax deductions arose for the taxpayer in the current tax period (i.e. i.e. the period for which the declaration is filled out).

In other words, column 3 reflects:

- tax amounts presented to the taxpayer upon acquisition of goods (work, services), property rights on the territory of the Russian Federation;

- the amount of tax paid by the buyer - tax agent when purchasing goods (work, services);

- amounts of tax presented to the taxpayer upon the acquisition in the territory of the Russian Federation of goods (works, services), property rights accepted for accounting in the period from January 1, 2007 to December 31, 2008 inclusive, and paid by him on the basis of a payment order for the transfer of funds funds for settlements with securities, barter transactions and offsets.

Line 010 in column 3 indicates the total amount of VAT accepted for deduction for each page of section. 5.

Line 010 = sum of column 3 indicators.

Columns 4 and 5 are intended to reflect the tax base and tax deductions for transactions for which the zero rate has not previously been confirmed. Columns 4 and 5 are filled in similarly to columns 2 and 3.

Line 010, column 5 indicates the total amount of VAT accepted for deduction for each page of section. 5.

Line 010 = sum of column 5 indicators.

The values of indicators in columns 3 and 5 of line 010 are involved in calculating the values of indicators of lines 040 and 050 of section. 1 declaration (paragraph 3, clause 34.3 and paragraph 2, clause 34.4 of the Procedure for filling out the declaration).

Section 6 “Calculation of the amount of tax on transactions involving the sale of goods (works, services), the validity of applying a tax rate of 0 percent for which is not documented.”

This section is filled out by taxpayers carrying out export operations, as well as work and services related to the production and sale of goods for export, who have not collected the required package of documents within the period established by paragraph. 1 clause 9 art. 165 of the Tax Code of the Russian Federation - within 180 days.

For the period from July 1, 2008 to March 31, 2010 inclusive, the period for confirmation of export is 270 calendar days. Corresponding changes have been made to clause 9 of Art. 165 of the Tax Code of the Russian Federation, clause 1, art. 1 of the Federal Law of December 27, 2009 N 368-FZ.

According to paragraph 3 of Art. 5 of Law No. 368-FZ provisions para. 6 clause 9 art. 165 and para. 4 paragraph 9 art. 167 of the Tax Code of the Russian Federation (as amended by Law No. 368-FZ) apply to legal relations that arose from 07/01/2008 and apply until 01/01/2011.

The moment of determining the tax base for the export of goods is the last day of the month in which the package of documents is collected (clause 9 of Article 167 of the Tax Code of the Russian Federation).

According to para. 2 clause 9 art. 165, para. 2 clause 9 art. 167 of the Tax Code of the Russian Federation, if within 180 days (in the period from 07/01/2008 to 01/01/2011 - 270 days) the taxpayer does not confirm the right to apply the 0% rate, i.e. does not collect a complete package of documents, he is obliged to charge VAT at a rate of 18%. The tax is calculated and paid no later than the 181st day from the date of placing the goods under the customs export regime, but for the tax period in which the shipment occurred, by submitting an updated VAT return (Article 81, paragraph 2, paragraph 9, Article 165 , paragraph 2, clause 9, article 167 of the Tax Code of the Russian Federation).

Section 6 is completed for the period when shipment occurred under an operation with an unconfirmed zero rate (paragraph 20, 24, paragraph 3 of the Procedure for filling out the declaration).

Column 1 reflects transaction codes in accordance with Appendix No. 1 to this Procedure.

Column 2 for each transaction code reflects the tax bases for transactions involving the sale of goods (works, services) taxed at a rate of 0%, the validity of which for these transactions is not documented. The tax base is equal to the cost of goods (work, services) sold.

Column 3 shows the VAT amounts for each transaction code.

Column 3 = column 2 x 18 (10) / 100.

For goods (works, services, property rights) acquired for the sale of exported goods (works, services), the taxpayer has the right to accept “input” VAT for deduction (clause 1, clause 2, article 171, clause 3, article 172 of the Tax Code of the Russian Federation ).

Column 4 reflects tax deductions for each transaction code, i.e. the amount of “input” VAT on goods (works, services, property rights) purchased for the sale of exported goods (works, services).

Column 4 reflects:

- tax amounts presented to the taxpayer upon acquisition of goods (work, services), property rights on the territory of the Russian Federation;

- amounts of tax paid when importing goods into the customs territory of the Russian Federation;

- the amount of tax paid by the buyer - tax agent when purchasing goods (work, services);

- amounts of tax presented to the taxpayer upon the acquisition in the territory of the Russian Federation of goods (works, services), property rights accepted for accounting in the period from January 1, 2007 to December 31, 2008 inclusive, and paid by him on the basis of a payment order for the transfer of funds funds for settlements with securities, barter transactions and offsets;

- tax amounts previously calculated from the amounts of payment received before January 1, 2006, partial payment for upcoming deliveries of goods (performance of work, provision of services), counted in the tax period when selling goods (work, services), justification for applying a tax rate of 0 percent for which there is no documented evidence.

On line 010, column 2 indicates the total amount of the tax base, column 3 - the total amount of tax, and column 4 - the total amount of tax deductions.

Line 010 column 2 = sum of column 2 indicators.

Line 010 column 3 = sum of column 3 indicators.

Line 010 column 4 = sum of column 4 indicators.

Line 020 reflects the amount of tax payable to the budget, and line 030 shows the amount of tax calculated for reduction.

If line 010 column 3 > line 010 column 4, then line 020 = line 010 column 3 - line 010 column 4.

If line 010 column 3 > line 010 column 4, then line 030 = line 010 column 4 - line 010 column 3.

The indicators of lines 020 and 030 are involved in calculating the indicators of lines 040 and 050 of section. 1 declaration (paragraph 3, clause 34.3 and paragraph 2, clause 34.4 of the Procedure for filling out the declaration).

Section 7 "Operations not subject to taxation (exempt from taxation); operations not recognized as an object of taxation; operations for the sale of goods (works, services), the place of sale of which is not recognized as the territory of the Russian Federation; as well as amounts of payment, partial payment on account of upcoming supply of goods (performance of work, provision of services), the duration of the production cycle of which is more than six months."

This section is filled out by taxpayers or tax agents who carry out operations:

- which are not subject to taxation (exempt from taxation) under Art. 149 Tax Code of the Russian Federation;

- not recognized as an object of taxation in accordance with paragraph 2 of Art. 146 Tax Code of the Russian Federation;

- if the place of sale of goods (works, services) is not the territory of the Russian Federation.

Section 7 is also completed by taxpayers (tax agents) if advance payments have been received for upcoming deliveries of goods (performance of work, provision of services) with a long production cycle.

In column 1, line 010, transaction codes are indicated in accordance with Appendix No. 1 to the Procedure for filling out the declaration.

Articles 146 and 149 of the Tax Code of the Russian Federation were supplemented by new provisions introduced by Federal Laws dated November 28, 2009 N 287-FZ and dated December 27, 2009 N 379-FZ.

In column 2, line 010, for each code of a non-taxable transaction and a transaction not recognized as an object of taxation, as well as transactions for the sale of goods (work, services), the place of sale of which is not recognized as the territory of the Russian Federation, the cost of the goods sold (transferred) is reflected. goods (works, services). The price is indicated without VAT.

For transactions that are not recognized as an object of taxation under Art. 146 of the Tax Code of the Russian Federation, and for operations the place of implementation of which is not recognized as the territory of the Russian Federation, columns 3 and 4 are not filled in (paragraph 3 of clause 44.2 of the Procedure for filling out the declaration).

In column 3, line 010, for each transaction code that is not subject to taxation, the cost of purchased goods (work, services) is reflected, the sales transactions of which are not subject to taxation in accordance with Art. 149 of the Tax Code of the Russian Federation, as well as the cost of goods (work, services) purchased from taxpayers who are exempt from fulfilling the duties of a taxpayer in accordance with Art. 145 of the Tax Code of the Russian Federation.

In column 4, line 010, for each transaction code that is not subject to taxation, the amounts of “input” VAT on the acquisition of goods (work, services) or paid when importing goods into the customs territory of the Russian Federation, which are not subject to deduction in accordance with clauses, are reflected. 2 and 5 tbsp. 170 Tax Code of the Russian Federation.

Line 020 reflects the amount of payment received, partial payment for upcoming deliveries of goods (performance of work, provision of services), the duration of the production cycle of which is more than six months, according to the list determined by the Government of the Russian Federation. This List was approved by Decree of the Government of the Russian Federation dated July 28, 2006 N 468.

At the same time, upon receipt of advance payments for upcoming deliveries of goods (performance of work, provision of services) with a long production cycle, in accordance with clause 13 of Art. 167 of the Tax Code of the Russian Federation, the taxpayer is obliged, simultaneously with the declaration, to submit a contract and a document confirming the duration of the production cycle of goods (works, services), indicating their name, production time, name of the manufacturing organization, issued to the specified taxpayer-manufacturer by the federal executive body exercising the functions of development of state policy and legal regulation in the field of industrial, defense-industrial and fuel-energy complexes, signed by an authorized person and certified by the seal of this body.

First, let's figure out what VAT is. Value added tax is a so-called consumption tax. In essence, such a tax is an addition to the price of the product being sold, that is, the buyer pays it when making a purchase. It is the enterprise that sells these products that submits the declaration to the inspectorate.

Various rates

The rate is regulated by Article 164 of the Tax Code of the Russian Federation; it is not fixed and differs for different types of goods.

For example, for most services and products the value added tax is 18%.

An exception is made for certain types of services and goods: children's products, books and periodicals of an educational nature, as well as some medical goods have a reduced rate of 10%. There is also a zero rate for exported goods, some passenger transport and others.

Tax agent - in what cases?

You may have encountered situations where a taxpayer, for some reason, could not pay tax on us himself, and another person did it for him (we will look at these cases below).

This is the tax agent who will deduct the required amount from income in advance and then send it to the state budget. Thus, this person or enterprise acts as a link between the state and this taxpayer.

According to the Tax Code, a tax agent for VAT is the one who:

- purchases products or services from foreign entities that are not registered with the Russian tax authorities (the purchase is made in Russia);

- rents or buys state property, property of constituent entities of the Russian Federation;

- sells confiscated goods, purchased valuables or buys the property of a bankrupt person.

VAT return - what is it?

A VAT tax return is a reporting document submitted by taxpayers indicating information about the amount of duties paid.